The Affordable Care Act has survived more than five years of nonstop challenges nearly intact. Yet even those inclined to endorse its sweeping benefits point out the act’s internal structure and external economics make it resemble a sand sculpture just above high tide far more than an immutable Stonehenge.

Deep recession. Big employers itching to get out of providing insurance. The elephant in the room of baby boomer retirements swelling Medicare costs beyond budget limits. All promise to alter what we at the moment consider the most important features of the ACA.

That humane expectation – that access to health care is more a right for the many than a privilege for the fortunate – has been embedded in Colorado’s collective psyche as much as it has been codified into state and federal law.

Adam Atherly, a professor and health care policy expert at the University of Colorado Denver, noted that when the Health Insurance Portability and Accountability Act passed in 1996, it was touted as a way for workers to keep their coverage while switching to a new job. Years later, the public perceives it as a firewall to protecting their electronic medical records from prying eyes.

“The privacy issue is what we talk about 20 years later,” Atherly said. “I have a feeling that what we will talk about in 20 years with the ACA, we don’t know yet.”

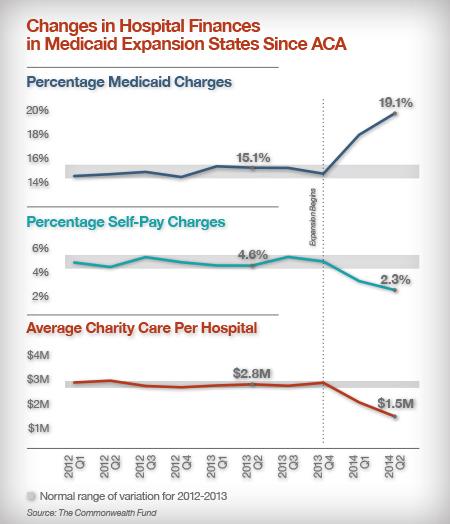

Most immediately, now that the U.S. Supreme Court has weighed in favor of federal subsidies in its crucial June decision, is a need to fix the Connect for Health Colorado insurance marketplace before all public and political confidence is lost, state experts agree. The exchange covers only about 140,000 people with individual policies compared with millions on employer-sponsored insurance plans, but its cost and its tenuous existence as a quasi-state agency give it outsized attention.

“It’s fair to say we do have a slight hit to the brand,” said interim exchange CEO Kevin Patterson, who as a longtime aide to Gov. John Hickenlooper is seen as a potential bridge between the exchange’s operations and what should be a close ally – state Medicaid. “When you only talk about problems, people think all you have are problems. When we look at the places where people get stuck, it’s less than 10 percent of those folks. The problem is, they are really, really stuck, and it’s frustrating as all get out. And you’re trying to make one of the most important purchases for your family. We’ve got to figure out a way to solve that problem.”

That answer won’t come until deep into the fall, when consumers trying to use the system learn whether the exchange and Medicaid interface was fixed, or whether ongoing problems continue to jam the costly call centers with time-consuming queries.

Consumers will also be learning about another deep worry of health insurance-watchers: what premiums will look like for 2016 policies in an atmosphere where newly insured clients may be using a lot of expensive services and driving up underwriting costs. In late spring of 2015, other states saw new rate filings in the high double digits, just like the “bad old days” of 2008 and 2009 before the ACA’s signing.

The Colorado Consumer Health Initiative, which watches rate filings and sometimes protests increases, said Colorado may be in a unique situation: The state has a high number of insurers competing in the marketplace, which tends to rein in rates, and some of the insurers have high surplus loss reserves they could use to keep rates low even if claims move higher.

Advocacy and analysis groups will turn slightly from promoting coverage – which a great many eligible Coloradans now have – to seeking better access to actual care for those now covered. Many areas of the state outside the large Front Range cities force Medicaid patients into long waits when they seek specialty appointments, noted Jandel Allen-Davis, MD, vice president of government and external relations for Kaiser Permanente Colorado. (Kaiser has about 52,000 of the state’s Medicaid clientele and sometimes has to cap further growth for financial and access reasons.)

“Specialty access is virtually impossible in some parts of the state,” she said. Medicaid officials will have to alter their reimbursement for specialty care if they want to break those logjams. “You don’t need just an insurance card – you need care.”

In Aspen late this spring, news surfaced that Pitkin County officials were searching hard for area providers who would take Medicaid, with some of the thousands of poverty-level residents having to go 70 miles to Rifle for care.

“You have to be careful where you assign blame for some issues,” said Joe Sammen, executive director of the Colorado Coalition for the Medically Underserved. “Specialty care access is a decades-long rural issue, not something necessarily that’s wrong with the law.”

Reform advocates see opportunity to broaden ACA benefits and win over new supporters by improving the performance of SHOP, the small employer insurance program meant to be promoted through the state marketplaces. SHOP lets the marketplaces channel federal tax credits to businesses or nonprofits with up to 50 employees who sign up for health coverage, but takeup has been extremely slow.

“We didn’t come close on enrollment targets in Colorado,” said Tim Gaudette, Colorado’s director of the Small Business Majority, an advocacy group. “It’s the second child, and it never saw the push and the emphasis.”

Without a mandate requiring small businesses to cover employees, it was too easy for employers to stay away when they heard of exchange glitches, Gaudette said. Brokers, meanwhile, did not find it a lucrative source of potential business. That could change, he added, when SHOP eligibility expands to 51 to 99 employees.

Specialty access is virtually impossible in some parts of the state. You don’t need just an insurance card – you need care.

“It’s not a slam dunk,” he said. “If it was easy, it would have been done a long time ago.”

The biggest wild card for health reformers – and the one mentioned least – is the certitude of a future recession that could threaten the coverage gains made possible by the ACA. The latest deep recession officially ended in June of 2009, and with recent recessions hitting every five to 10 years, the U.S. would be due for a downturn by the end of this decade.

“Absolutely another recession will happen,” Atherly said. When it does, states like Colorado with tight restrictions on raising taxes or shifting budget burdens will seek relief in health costs, now making up about a third of general fund spending in many states through the growth of Medicaid programs. (Traditionally Medicaid is half funded by the federal government, and for now, Medicaid expansion is paid 100 percent by federal funds. The federal share for those new clients drops to 90 percent in coming years.)

Colorado’s hospital provider fee offers some cushion in a recession to pay for the state’s portion of Medicaid. And ACA rules about the Medicaid expansion include a bar on states cutting back eligibility once they have accepted the expansion. But other health costs can still be attacked, including Medicaid reimbursement rates to hospitals and other providers, Atherly noted. In one recession, he said, Hawaii started limiting inpatient hospital days. “A lot of states will try to do some pretty radical things,” he said.

Nationally, a recession would cut into tax collections and put pressure on Congress to cut the Medicaid expansion, alter Medicare and slash marketplace insurance subsidies, among other moves.

“I’d say no, the system’s not prepared for another recession,” Sammen said. “But is any system?”

This article was originally published in the Summer 2015 issue of Health Elevations.